Market volatility is nothing new. In fact, the S&P 500 has averaged a 14% correction every year since 1980, even in years when the market ultimately finished strong. These pullbacks can feel jarring, especially when they're accompanied by grim headlines and emotional market swings. But here's the truth: corrections are a normal part of the market cycle, and history rewards those who stay the course.

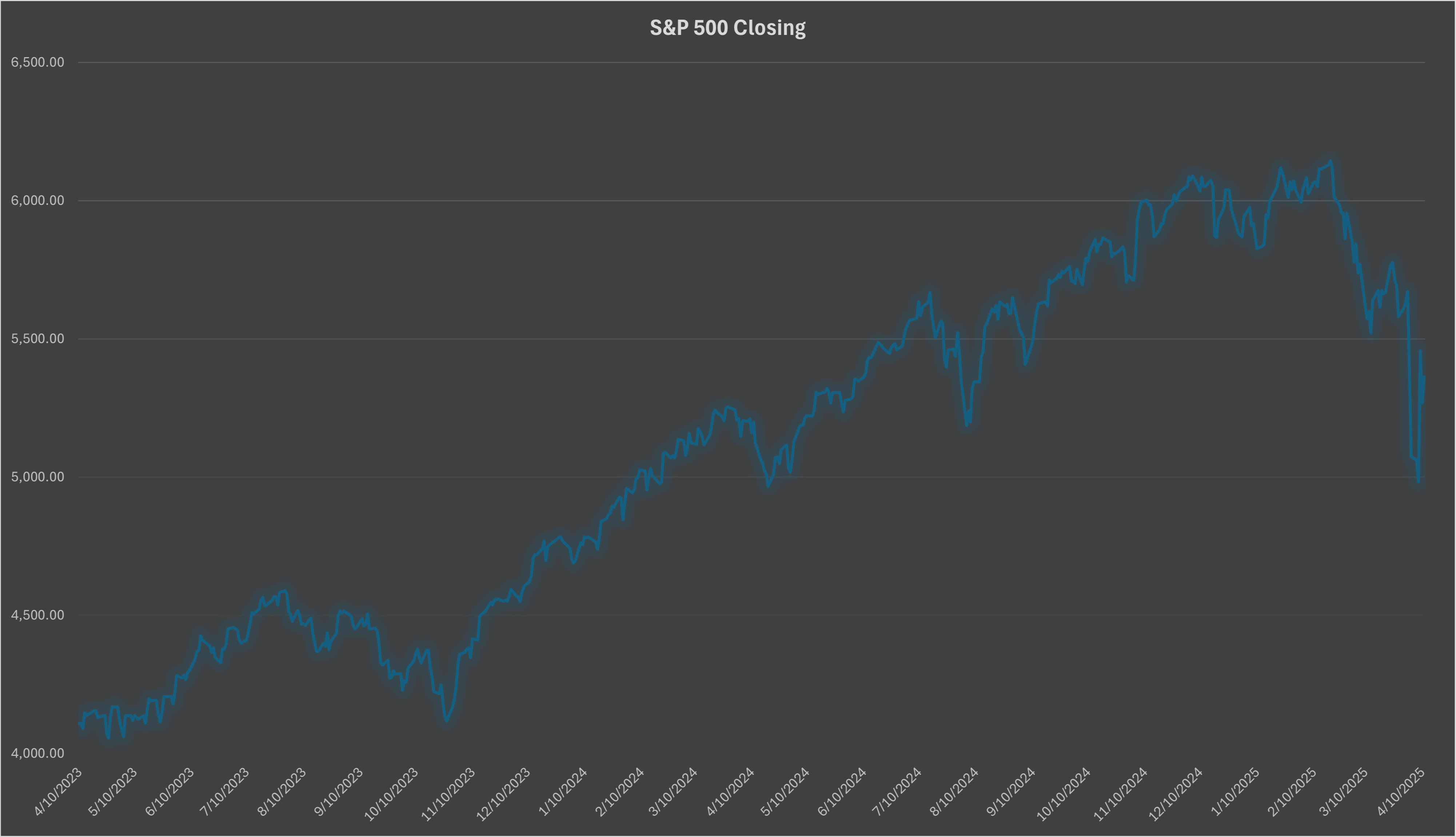

S&P 500 Historical Data by MarketWatch. Market Closing, April 10 2023 through April 10 2025

A Look at Real Corrections

Let’s start with a few historical examples:

- 1987 (Black Monday): The S&P 500 dropped 33.5% between August 25 and December 4, including a single-day plunge of 20.5%. Yet within 20 months, the index had fully recovered.

- 2018: A 19.8% drop from September to December amid Fed rate hike fears. The market rebounded fully by April 2019.

- 2020 (COVID-19): In just 33 days, the market lost 33.9% of its value. Yet by late August 2020, it had reclaimed its previous high.

These are just a few of over two dozen S&P 500 corrections and bear markets since 1980. Downloadable data from Yardeni Research offers a comprehensive table if you want to explore every drawdown and recovery.

The Cost of Getting Out

When volatility hits, it's tempting to "get out and wait for the storm to pass." The problem isn't getting out—it's getting back in. Markets often rebound sharply, and missing just a few of the best-performing days can affect long-term returns.

For example:

- From 1995 to 2014, the S&P 500 averaged 9.85% annually. Miss just the 10 best days? Your return drops to 6.1%.

In other words, most annualized gains come from a handful of trading days — days you’re likely to miss if you're on the sidelines.

Emotional Investing: The Real Risk

Behavioral finance tells us something we already know in our gut: losses hurt more than gains help. In fact, research shows that we feel the pain of a loss 2 to 2.5 times more intensely than the pleasure of a gain. This emotional imbalance causes investors to overreact to short-term declines, often abandoning their long-term plan at the worst possible moment.

DALBAR’s 2023 Quantitative Analysis of Investor Behavior found that the average equity investor underperformed the S&P 500 by over 5% annually, largely due to mistimed buy/sell decisions. People sell low, buy high, and repeat.

The irony? Corrections often precede some of the best market days. Selling out of fear means you’re almost certain to miss the bounce.

Diversification, Rebalancing, and Recovery

Having a well-diversified portfolio helps smooth the ride. Annual rebalancing ensures you don’t drift too far from your long-term targets. But beyond the math, it helps psychologically. Knowing you have a strategy in place makes it easier to stay calm when the headlines are anything but.

Recovery strategies matter too. Instead of retreating during a correction, seasoned investors look for opportunities—quality assets that are temporarily discounted.

The Value of a Financial Professional

Plenty of people say, “I manage my own money.” And in bull markets, that might work. But during downturns, the true value of a financial professional shines through. Vanguard’s "Advisor’s Alpha" study estimates that behavioral coaching alone can add +3% annually to a client’s returns—simply by helping them avoid costly emotional mistakes.

Russell Investments echoes this, calling the advisor a critical "behavior coach." Having someone in your corner to say, “This too shall pass,” backed by decades of market data, isn’t just comforting—it builds confidence.

Final Thoughts

The market doesn’t have feelings, but investors do. And in a world with shrinking attention spans and 24/7 news cycles, it’s easy to let fear drive decisions. But if history teaches us anything, it’s that those who stay the course are rewarded.

The next time you see an 8% drop in a week, remember: the average market correction is 14% per year. It's not a reason to panic—it's part of the process.

If you're not sure how to weather the storm or want to review your strategy, reach out. This is exactly why working with a financial advisor can make a difference.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.